$600 Billion Gap – Is the AI Bubble Going to Burst? A Case Study

Why your MacBook just got more expensive, why a 25-person startup dumped Anthropic, why Wall Street’s smartest investors can’t agree on what’s happening, and is the AI bubble going to burst?

Here’s a strange fact to start with. On June 25, 2026, Apple did something it had never done in its entire history. In the middle of the year, with no new product launch, no new iPhone, nothing, Apple simply raised its prices.

The MacBook Air went up. The iPad Pro went up by as much as 20%. Even the Apple TV jumped. And when people asked “why now?”, Apple said something they have never said before:

“We have never seen a component price increase this much, this quickly.” Apple, in an official statement

The reason isn’t inflation, or tariffs, or a new chip design. It’s a war being fought over tiny memory chips, thousands of kilometers away, in factories in South Korea. And that war has one cause: artificial intelligence.

This is the story of the biggest financial bet humanity has ever made, and why, in June 2026, cracks started to show. By the end of this case study, you’ll understand this topic better than most people talking about it on the internet. Let’s get into it.

What a Data Center Actually Is

Before we look at any scary numbers, let’s build a simple picture in your head. Because if you don’t understand what a data center really is, none of the billions of dollars will make sense.

Think about your phone. When you type a question into ChatGPT, your phone doesn’t actually “think” for you. Your phone is just a screen with Wi-Fi. The real thinking happens somewhere else, inside a giant, windowless warehouse packed with metal racks. Each rack holds thousands of computer chips. That warehouse is a data center.

One of these buildings can hold up to 100,000 Nvidia GPUs (graphics chips built for AI). Each GPU costs $30,000 to $40,000. That means one building alone can hold $3 to $4 billion worth of chips, and that’s before you add the cooling systems, the power supply, the high-speed cables, the concrete, and the fire safety systems. All in, one large AI data center costs $10 to $25 billion to build.

Now multiply that by hundreds of data centers being built across the US right now, and you start to understand the scale of the bet.

Want to certify your AWS AI skills? Get 200+ PDF Practice Questions for AWS AI Practitioner Exam and get certified on your first attempt.

The Numbers That Should Scare You

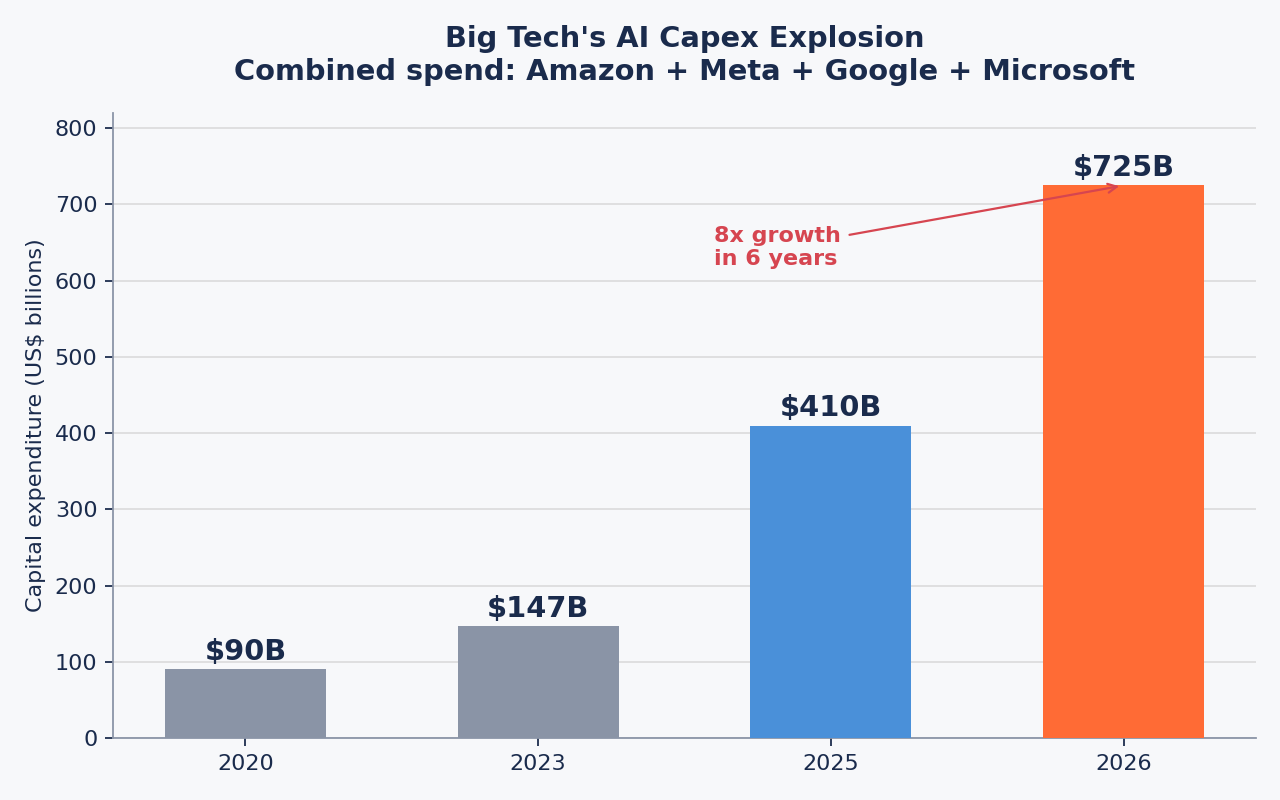

Let’s look at how fast the spending has grown. In 2020, before ChatGPT even existed, the four biggest US tech companies, Amazon, Meta, Google, and Microsoft, spent a combined $90 billion on capital expenditure (that’s money spent on physical infrastructure, like data centers).

- In 2023: $147 billion

- In 2025: $410 billion

- In 2026: $725 billion

That’s an 8x increase in just six years, all funded by just four companies.

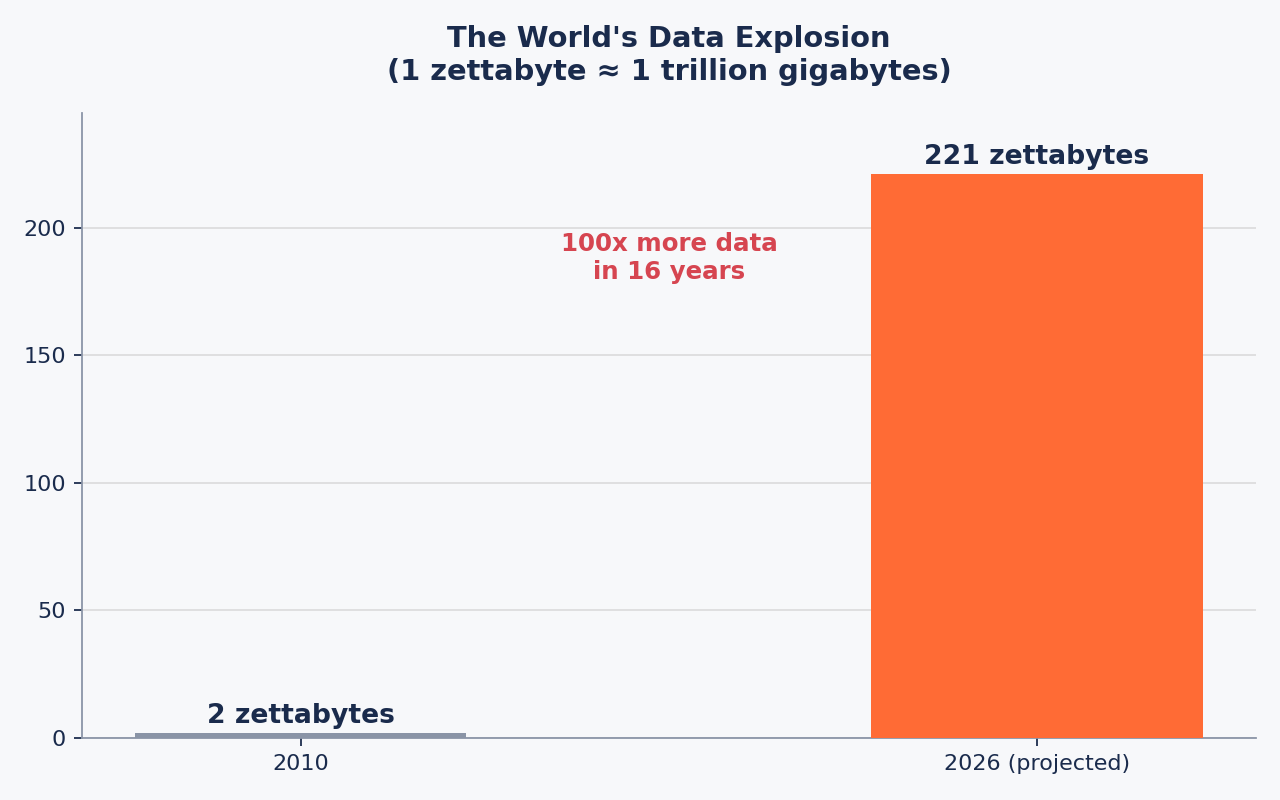

Why is all this spending happening? Because the amount of data the world creates has exploded. In 2010, the world created about 2 zettabytes of data (a zettabyte is roughly 1 trillion gigabytes). By 2026, that number is projected to hit 221 zettabytes, more than 100 times more.

Here’s the number that should really make you pause. According to a PIMCO report, over the next two years, Big Tech’s AI-related capital spending will consume 94% of their operating cash flow. In simple words, for every $100 these companies earn, they are putting $94 straight back into building AI infrastructure. Back in 2023, that ratio was just 40%.

That means Big Tech is betting almost all of its money on one single assumption: that in a few years, the world will need so much AI computing power that today’s spending will look cheap in comparison.

Sounds bold, right? Well, here’s where it gets uncomfortable.

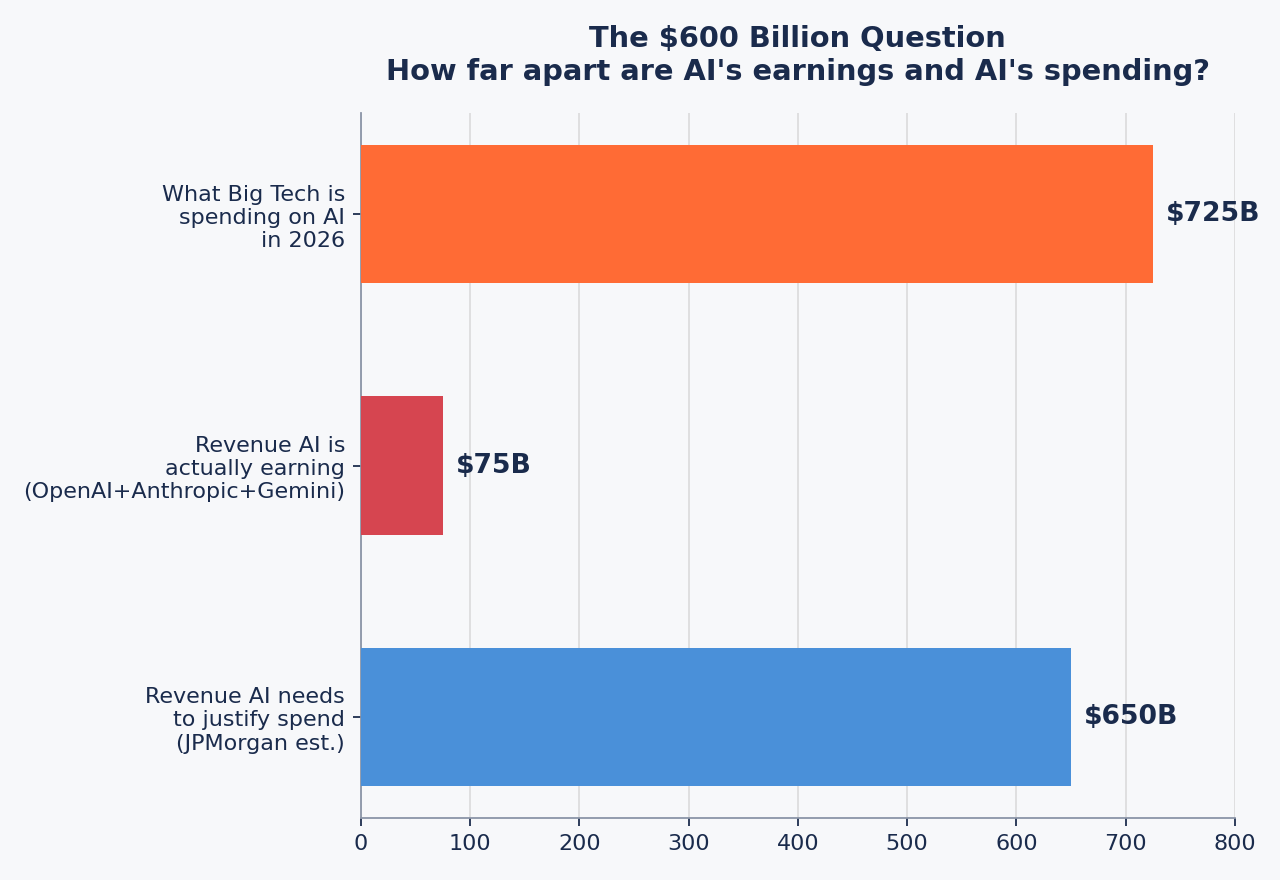

The $600 Billion Question

Let’s do a simple thought experiment. Imagine you spend $10 million building a coffee machine factory. After a year, your factory only sells $400,000 worth of coffee machines. Is that good, bad, or terrible?

It’s terrible. Nobody would build a second factory on numbers like that.

Now apply the exact same logic to AI. This calculation was actually done by JP Morgan, and later made famous by David Cahn, a partner at Sequoia Capital, in an essay called “AI’s $600B Question.” The logic is simple: if you’re an investor putting money into something, you’d want at least a 10% return. So Cahn asked, How much revenue does the AI industry actually need to bring in every year to justify the spending?

The answer: around $650 billion a year.

Now let’s check how much AI companies are actually earning:

- OpenAI: makes about $25 billion a year, but is losing around $14 billion a year

- Anthropic: on track for roughly $26 billion this year (with an optimistic best-case of $47 billion), and reportedly lost money in 2025

- Google Gemini: roughly $25 billion

Add it up, and the whole AI industry earns somewhere around $75 billion a year. Compare that to the $650 billion it needs to earn, and to the $725 billion Big Tech is spending on infrastructure every year.

That’s roughly a 9 to 10x gap between what the AI industry earns and what it needs to earn to justify the spending. This is why some analysts, like SEOA’s David Cahn, call this “AI’s $600 billion question” a massive annual revenue gap, and nobody quite knows who is going to fill it.

The obvious counter-argument is: “Enterprises will pay eventually, once AI makes them efficient enough.” Except… the data doesn’t support that yet.

- McKinsey found that 73% of enterprise AI deployments are failing to achieve their expected return on investment.

- BCG found that only about 5% of companies are seeing substantial ROI from AI.

- MIT’s widely-cited “GenAI Divide” report found that around 95% of enterprise generative AI pilots fail to deliver measurable financial return.

- Only 29% of executives can even properly measure their AI return on investment.

This is where the story gets its first real plot twist.

Meet Flo: The Startup That Blew Up the Model

Meet Flo Crivello. He runs a 25-person AI startup in San Francisco called Lindy. In June 2026, he gave an interview that shook the industry.

His company’s AI bill, specifically for using Anthropic’s Claude models, had grown bigger than his entire payroll. So what did he do? He switched 100% of Lindy’s traffic to DeepSeek, a cheaper Chinese AI model. His costs “crashed to the ground,” and he said the move would save the company millions of dollars.

“We did it, and you could see that cost curve go down, like, crash to the ground.” Flo Crivello, CEO of Lindy, to CNBC

Crivello was blunt about why: “It’s a matter of survival for the business.” He also said on X that after the switch, he actually saw better performance on many of Lindy’s core tasks, not worse.

Around the same time, Uber’s CTO admitted publicly that Uber had blown through its entire annual AI budget in just four months, according to CNBC’s reporting.

This matters because the whole business model of companies like OpenAI (valued around $850 billion) and Anthropic (valued around $965 billion) was built on the assumption that enterprises would keep paying more and more for AI tokens, forever. In June and July 2026, that assumption started to crack, enterprises began actively hunting for cheaper alternatives, and cheaper Chinese open-weight models like DeepSeek and Z.ai’s GLM 5.2 started eating into market share fast, according to CNBC.

Palantir’s CEO Loses It on Live TV

If you want proof that answers the key question, is the AI bubble going to burst, and explains this isn’t just a “rich person’s problem,” look at what happened on July 1, 2026, when Palantir CEO Alex Karp appeared on CNBC’s Squawk Box.

Palantir is one of the biggest enterprise software companies on Earth. They sell to the CIA, the US government, Airbnb, JP Morgan, and dozens of other massive organizations. So when its CEO goes on live television and says the AI industry has gone completely wrong, people listen.

“Every single enterprise I deal with, they’re like, ‘I am paying for tokens that create no value. These people are stealing the weights and alpha of my business, and they’re creating a wealth tax.'” Alex Karp, CEO of Palantir, on CNBC

Karp argued that leading AI labs had “completely, irresponsibly” oversold their models to enterprises, charging heavily for token usage while quietly harvesting the client’s own data to improve their own products. When a CNBC host said he sounded angry, Karp replied: “This is the voice of American business that is being channeled through me.”

Interestingly, Palantir’s own stock jumped more than 9% that same day, so investors weren’t exactly punishing him for saying it.

How You’re Already Paying the “AI Tax”

Now, you might be thinking: “Okay, Nvidia losing hundreds of billions, Sam Altman, Dario Amodei, Sundar Pichai, they’re all billionaires. How does this affect me?”

Let’s go to South Korea to answer that.

There’s a Samsung factory there that produces DRAM, the memory chips that go into your laptop, your phone, your Xbox, and even your washing machine. In 2024, Samsung had a choice: sell that memory to regular consumer companies like Apple, HP, or Dell, or sell a special, much more expensive version called High Bandwidth Memory (HBM) to AI data centers.

Guess which one paid more? AI data centers paid 10 times more per module. So Samsung, SK Hynix, and Micron, the three companies that control about 90% of the world’s memory chip supply, did what any factory would do: they shifted roughly 93% of their production toward AI memory chips. Capital always flows to the highest bidder.

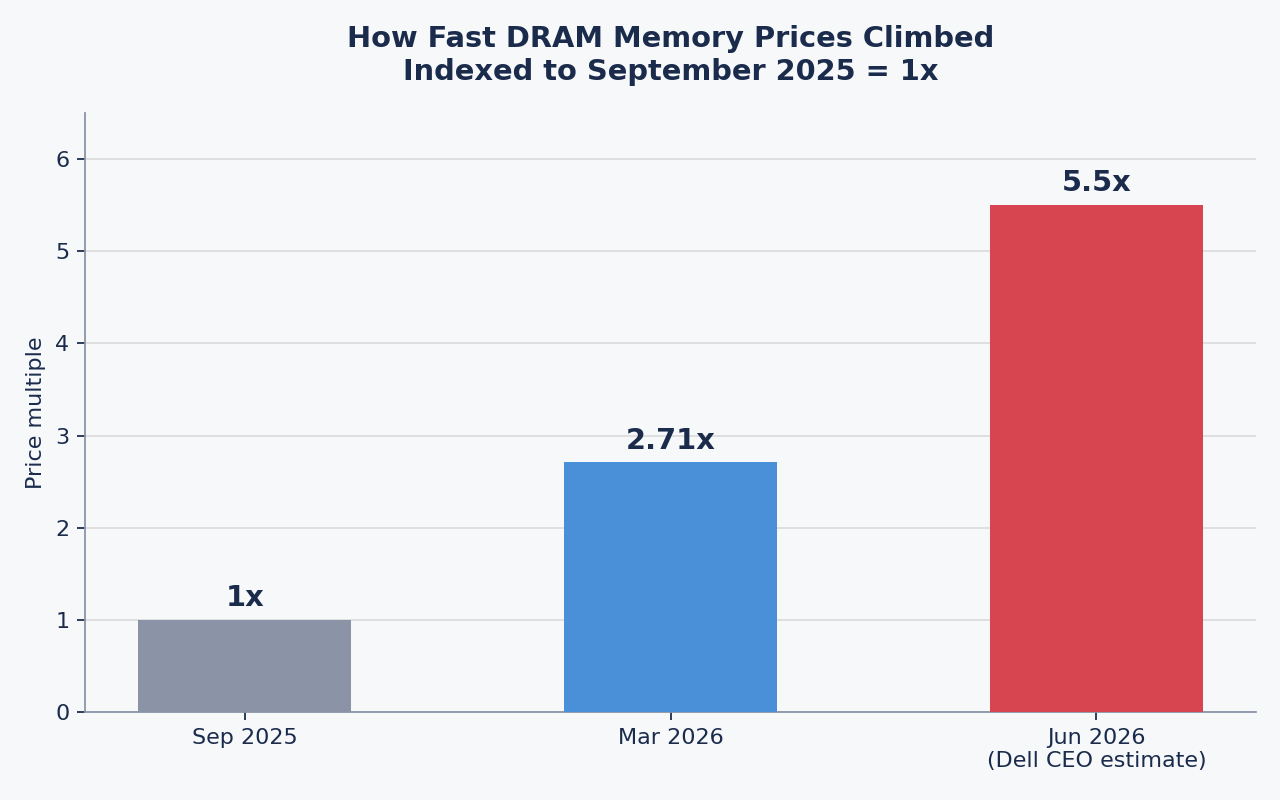

The result? DRAM prices are up 171% year-over-year as of March 2026. DDR5 memory prices are up 4x since September 2025. A contract price for PC memory jumped by 105 to 110% in a single quarter. Dell’s CEO said the price of 1 GB of DRAM went from $0.43 to $2.39 in just six months,a 5.5x increase.

That is exactly why, on June 25, 2026, Apple raised prices on Macs, iPads, home devices, and even the Vision Pro. As Apple’s official statement to the press put it:

“We’ve shielded our customers from these increases so far, but now we’ve reached a point where we need to begin raising prices.”

The base 13-inch MacBook Air jumped from $1,099 to $1,299. The entry MacBook Pro jumped $300 to $1,999. Even the Mac Studio jumped over $1,000, according to Bloomberg. Apple’s stock fell more than 6% the same day, its worst single-day drop in over a year, per CNN.

That is how you, someone who has never touched an Nvidia GPU in your life, are paying for the AI boom. It’s baked into the price of your next laptop.

The Capital Cycle: Why Everyone Keeps Spending Anyway

Here’s the confusing part. If enterprises are switching away from expensive AI models to save money, and if Apple can’t even absorb rising chip costs anymore, why on earth are Amazon, Microsoft, Google, and Meta still spending more?

The answer lies in one of the most useful concepts in economics: the capital cycle. It explains almost every bubble in modern history, and it works in four steps:

- High returns attract capital. Investors see a hot new sector making great returns, and money floods in.

- Capital keeps flowing until overcapacity is built. Everyone wants a piece, so more and more gets built, often more than is actually needed.

- Overcapacity leads to collapse. Prices crash because there’s too much supply and not enough demand to match it.

- Only a few survivors remain, and they eventually make a fortune once real demand finally catches up.

This exact pattern played out with railroads in the 1800s. It played out with the internet in the late 1990s. And it might be playing out again with AI right now.

History Repeats: The Dot-Com Warning

Let’s go back to 1996. The US passed the Telecommunications Act because, just like AI today, the internet was seen as a life-changing technology with explosive demand. Some founders genuinely believed internet traffic would double every three months. Money poured in to lay fiber optic cables across the country. In just five years, telecom companies invested more than $500 billion into cables, switches, and networks.

Look at how similar the financial story sounds to what’s happening with AI now:

- Global Crossing went from a small equity check to a $47 billion valuation without ever posting a single year of profit.

- Corvis, a fiber equipment startup, pulled off a $1.1 billion IPO with zero revenue and carried a $32 billion market cap.

Then the collapse came. Everyone had expected internet traffic to grow by 1,000% a year. It actually grew by “only” 100% a year — impressive, but nowhere near enough to justify the investment. Guess how much of that installed fiber cable was actually being used by the early 2000s? Just 2.7%. Over 95% sat completely unused, buried underground.

Bandwidth prices crashed by up to 90%. WorldCom, after hiding $3.8 billion in expenses to fake profits, filed the biggest bankruptcy in US history at the time. Global Crossing, that $47 billion darling, went bankrupt. In total, the telecom crash wiped out $2 trillion in market value, with stocks falling by up to 95%.

But here’s the twist that makes this the perfect mirror for AI: those fiber optic cables didn’t disappear. They sat in the ground, and a few years later, real demand finally arrived — YouTube, streaming, cloud storage, smartphones. Survivors bought the wrecked infrastructure for pennies on the dollar, and that “wasted” cable became the actual backbone of the modern internet, the same infrastructure that made Google, Netflix, and AWS possible.

So yes, the technology was real. The internet did change everything. But the bubble still burst, because demand was growing fast, but not fast enough to justify how much capacity had been built. The technology survived. Most of the companies that built it did not.

This pattern isn’t new either. Britain in 1846 authorized 9,500 miles of railway track, and about one-third of it never got built before that bubble burst, too. In 2026, America alone is building $725 billion worth of data centers every year, and nobody yet knows how much of it will actually get used.

So… Is the AI Bubble Going to Burst?

Here’s the honest answer: we don’t know for certain yet. And anyone who tells you they know for sure — in either direction — probably isn’t being fully honest with you.

There are real differences between this AI boom and the dot-com crash:

- The telecom companies in 2000 were funded heavily by debt and were losing money. NVIDIA, on the other hand, earned about $120 billion in net income last year. Microsoft, Google, and Amazon are some of the most profitable companies in human history — they won’t simply collapse the way weaker companies did.

- At the peak of the dot-com bubble, the Nasdaq 100’s forward price-to-earnings ratio was around 60x. Today it’s around 26x — higher than normal, but nowhere near 1999-level insanity.

At the same time, some of the smartest investors in the world are sounding alarms. Billionaire investor Ray Dalio, founder of Bridgewater Associates, said in a Bloomberg TV interview:

“All great technology changes produce bubbles. Nobody can get it exactly right.” Ray Dalio, Bloomberg Television

Dalio has separately said he views the AI bubble as being at roughly “80% of the euphoria” that led up to the 1929 crash or the 2000 dot-com crash, which is a striking thing for someone of his stature to say out loud. Investors like Michael Burry (famous for predicting the 2008 housing crash) and business figures like Jeff Bezos have made similar comments, comparing the current AI investment mania to past industrial bubbles.

Also worth remembering: Nvidia briefly became the first company in history to reach a $5 trillion market cap in late 2025, and again in early June 2026. Just a few days later, tech stocks got hit hard. By June 24, Micron and SanDisk had tumbled sharply, Apple fell over 6%, and SoftBank dropped around 12% in the same rough window, while OpenAI reportedly delayed its planned IPO.

The truth, uncomfortably, sits somewhere in the middle. There is a very high possibility of an AI bubble burst, but it’s not a certainty. The technology is real. Some of the revenue is real. But this isn’t really a debate about whether AI will change the world, most serious people agree it probably will. The actual debate is about whether the current price tag on that future makes sense.

What Happens Next

So where does this leave us? There are basically two roads ahead.

Path One: The bubble pops. Jobs get lost, the Nasdaq drops sharply, and big tech companies slam the brakes on spending. This matters a lot outside Silicon Valley, too, that spending is part of what feeds sectors like IT services and outsourcing around the world. If capex spending stops suddenly, a lot of that trickle-down work disappears with it.

Path Two: The bubble doesn’t pop — but prices go up instead. To justify their trillion-dollar valuations, AI companies race toward profitability by raising prices. Token costs (the price of actually using AI) go up, and only the biggest companies can afford the best AI. The cheap, almost-free AI tools many of us use today could slowly become a luxury. In this version of the story, some AI products don’t die because the technology failed, they die because it simply became too expensive to run.

There’s technically a third, much less likely path: some kind of efficiency miracle that drops the cost of running AI dramatically, lets enterprises actually turn a profit from it, and everybody wins. It’s possible. It’s just a very small possibility right now.

Whichever path we’re on, one thing is already true today: the AI boom is no longer just a Silicon Valley story. It’s showing up in your Apple bill, in your cousin’s job search, and in the prices tagged on your next laptop. Whether history remembers 2026 as the year of the greatest business bet ever made, or the year the greatest bubble in history started cracking, that part, only time will tell.

Quick FAQ: The AI Bubble in Plain English

Is AI itself fake or overhyped?

No. This isn’t a story about AI not working. Millions of people use AI tools every day, and many businesses genuinely save time and money with them. The debate is not “does AI work,” it’s “does the current price tag on AI infrastructure make financial sense.” Those are two very different questions, and it’s easy to mix them up.

Why does a memory chip shortage matter to someone who doesn’t use AI at all?

Because DRAM and NAND memory chips go into almost every piece of consumer electronics, laptops, phones, game consoles, smart TVs, even washing machines. When AI data centers start buying up the world’s memory supply at 10x the normal price, chip makers redirect their factories toward AI customers. That leaves less supply, and higher prices, for everyone else. It’s simple supply and demand, just playing out at a massive scale.

If big AI companies are losing money, why are their valuations so high?

Valuations in these situations are usually based on future expectations, not current profit. Investors are betting that AI companies will eventually become extremely profitable once the technology matures, adoption grows, and costs come down. That bet might turn out to be right. It might not. That uncertainty is exactly why terms like “bubble” keep coming up.

Is the AI bubble going to burst?

Nobody, not Ray Dalio, not JP Morgan, not this blog post, can tell you with certainty whether AI stocks will keep climbing or whether a correction is coming. What’s useful is understanding the mechanics behind the headlines: capital cycles, revenue gaps, and how infrastructure spending works, so that you can form your own judgment instead of just reacting to hype or panic.

Why This Story Matters Beyond Silicon Valley

It’s tempting to treat all of this as a rich-people problem. Billionaires are losing paper wealth on stocks most of us don’t own. But the ripple effects reach much further than Wall Street.

Take the global IT and services sector as one example. A huge amount of outsourcing, coding work, and back-office support work is downstream of exactly the kind of capital spending we’ve been talking about. When large US tech companies pour hundreds of billions into infrastructure, some of that spending flows into contracts, projects, and hiring across the world. If that spending suddenly slows down because the AI bubble burst scenario plays out, entry-level tech jobs, the kind fresh graduates are counting on, can disappear before the boom even reaches them.

On the flip side, if AI token prices keep climbing because companies are racing to become profitable, the cheap, almost-free AI tools that startups, students, and small businesses currently rely on could become considerably more expensive. That would change who gets to benefit from AI in the first place, shifting it from something broadly accessible to something only larger, well-funded organizations can comfortably afford.

Either way, the outcome of this “bet” doesn’t stay contained inside a handful of trillion-dollar companies. It shapes hiring, pricing, and access to technology far beyond the boardrooms where the actual decisions are being made.

Sources referenced in this post

- CNN — Apple hikes the prices of MacBooks and iPads because of memory chip shortage

- PBS News — Apple increases prices for Macs and iPads, blaming memory chip shortage fueled by AI

- Bloomberg — Apple Hikes Mac, iPad Prices on Memory Shortage; Shares Fall

- Sequoia Capital — David Cahn, “AI’s $600B Question”

- Fortune — MIT report: 95% of generative AI pilots at companies are failing

- CNBC — OpenAI and Anthropic face new AI reality as users shift from ‘tokenmaxxing’ to efficiency

- CNBC — Chinese AI models are gaining ground with U.S. companies as OpenAI, Anthropic costs surge

- Forbes — Palantir Billionaire Alex Karp Calls AI Industry ‘Effing Insane’ In Heated Interview

- MarketScale — Enterprise AI hits an inflection point as companies rein in spending

- Bloomberg — Dalio Sees AI Bubble Bursting as Wealth Is Converted Into Money

- Fortune — Ray Dalio warns AI is in the early stages of a bubble

- Morningstar — As Nvidia Crosses $5 Trillion, 5 Charts on the Unstoppable Tech Rally

- CNBC — Stock market news for June 24, 2026

Note: This post is for informational purposes only and is not financial advice.